Floor Plan Lending Ucc

The U C C Churches Have Been Focusing On Going Green So We Decided To Build Our Library Little Free Libraries Little Free Library Plans Free Library

What Is A Ucc Filing How A Ucc Lien Works Willcox Buyck Williams

How Can A Ucc 1 Blanket Lien Affect Your Business

Office Building Floor Plan Hingham Congregational Churchhingham Congregational Church

Ucc Financing Statement Collateral Description Fundamentals Csc

Ucc 128 Bar Code Labels What Are They How To Print These Labels Barcode Labels Shipping Labels Labels

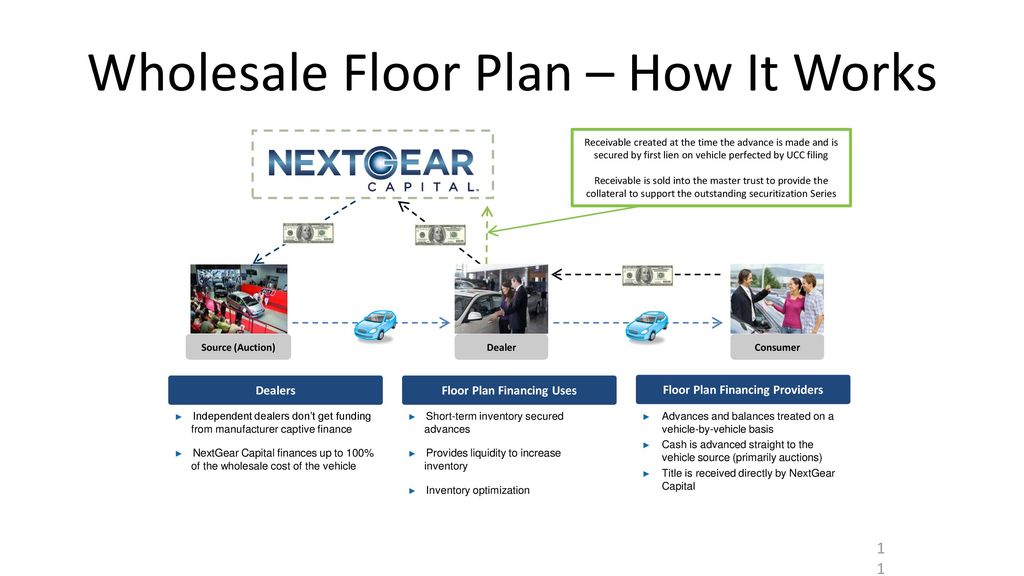

In order to facilitate the ability of lenders to floor plan or otherwise finance the acquisition of inventory by dealers of titled equipment the ucc in almost all states provides that filing a financing statement is the proper method of perfection d uring any period in which collateral subject to a state certificate of title law is.

Floor plan lending ucc.

Get Low Cost Merchant Cash Advance Leads To Reap Huge Profits Lead Generation Marketing Cash Advance Lead Generation

Dealer Funding Good Afternoon I Am Susan Moritz Vice President Of Development For Nextgear Capital The Focus Of This Workshop Is Leveraging Inventory Ppt Download

Ucc Frequently Asked Questions Tennessee Secretary Of State

What Is A Ucc 1 Filing How Do Ucc Liens Work Valuepenguin

Source : pinterest.com